Warburg Pincus is exploring a sale of the Group at a headline above $1bn while its own implied IRR on a $1.1bn exit is approximately 18% — seven points below the 25% institutional LP threshold. This creates structural sell-side urgency that compresses the negotiating window to H2 2026 and exposes the Group to a transaction at $1.20–1.30bn when its underlying technology and competitive position support $1.40–1.60bn.

Institutional Pulse

McGill & Partners enters the most consequential 180 days in its six-year history. The Group is simultaneously: at the outer edge of its sponsor's hold cycle, executing a technology transformation unmatched among mid-market specialty brokers, operating in a competitive set in which every primary rival is structurally distressed, and approaching three concurrent regulatory deadlines whose resolution will determine whether the inevitable transaction closes at platform multiples or broker multiples. The underlying business is operating at peak quality. The transaction infrastructure surrounding it is not.

What the rings reveal

Ring 1 · Strategic Health (78). Strong financial trajectory and technology moat, dragged by the unresolved AIG change-of-control single-point vulnerability. Resolve neutral and the score lifts to 86 within 30 days.

Ring 2 · Web Presence (44). The widest gap in the report. Site is technically modern, strategically silent. Communicates 30–35% of actual market position. 90-day intervention can close 60–70% of the gap.

Ring 3 · Market Position (81). The most favourable competitive position in the segment for the H2 2026 → H1 2027 window. Every primary rival structurally distressed.

Ring 4 · Operational Readiness (62). The only thing standing between intrinsic platform-quality position and a transaction at platform multiples. Closing the gap inside 90 days lifts above 75.

AIG change-of-control provision contains a termination right; bidders apply broker multiples; sale closes at the lower end of the comparable range. Digital brand programme not executed before IM distribution.

AIG provision neutralised; digital brand programme executed; founder commitment signed; Ryan Specialty closes the transaction in Q1–Q2 2027 with a 6-month FCA timeline.

Ryan Specialty competes against a wildcard (Tokio Marine / Marsh / Gallagher); platform narrative fully documented; auction extracts a tech-enabled platform multiple.

Probability-Weighted Enterprise Value

| Scenario | Probability | EV | Contribution |

|---|---|---|---|

| Bear | 20% | $880m | $176m |

| Base | 55% | $1.30bn | $715m |

| Bull | 25% | $1,650m | $413m |

| Probability-Weighted EV | 100% | $1.30bn |

Resolve the AIG-Palantir change-of-control provision

Single contractual question worth $200–300m of enterprise value at the bid stage.

Mandate financial adviser; begin FCA s178 pre-notification

The 5–9 month FCA timeline governs every closing date downstream of process launch.

Execute the 60-day digital brand programme

Owned digital channel currently undermines the platform-multiple thesis. Worth $150–250m of valuation framing.

Document founder commitment beyond transaction

Signed 3–5 year letter, available in data room, lifts the closing multiple by approximately one full turn.

Commission DORA & EU AI Act compliance programmes

17-week minimum project window for EU AI Act conformity assessment ahead of August 2026 enforcement.

Board Priorities — 90-Day Window

| Priority | Owner | Window |

|---|---|---|

| Confirm AIG-Palantir contract terms (change-of-control, exclusivity, term) | General Counsel + CEO | 30 days |

| Mandate financial adviser; begin FCA s178 pre-notification | Chair + CFO | 30 days |

| Build /platform technology page; fix domain redirect | CMO + Head of Technology | 30 days |

| Founder commitment letter signed and circulated to bidders | Chair | 60 days |

| DORA Register of Information filing for Irish entity confirmed compliant | General Counsel | 60 days |

| Top-50 producer retention package designed | CEO + CHRO | 90 days |

Verdict

Named Primary Acquirer — Ryan Specialty (NYSE: RYAN)

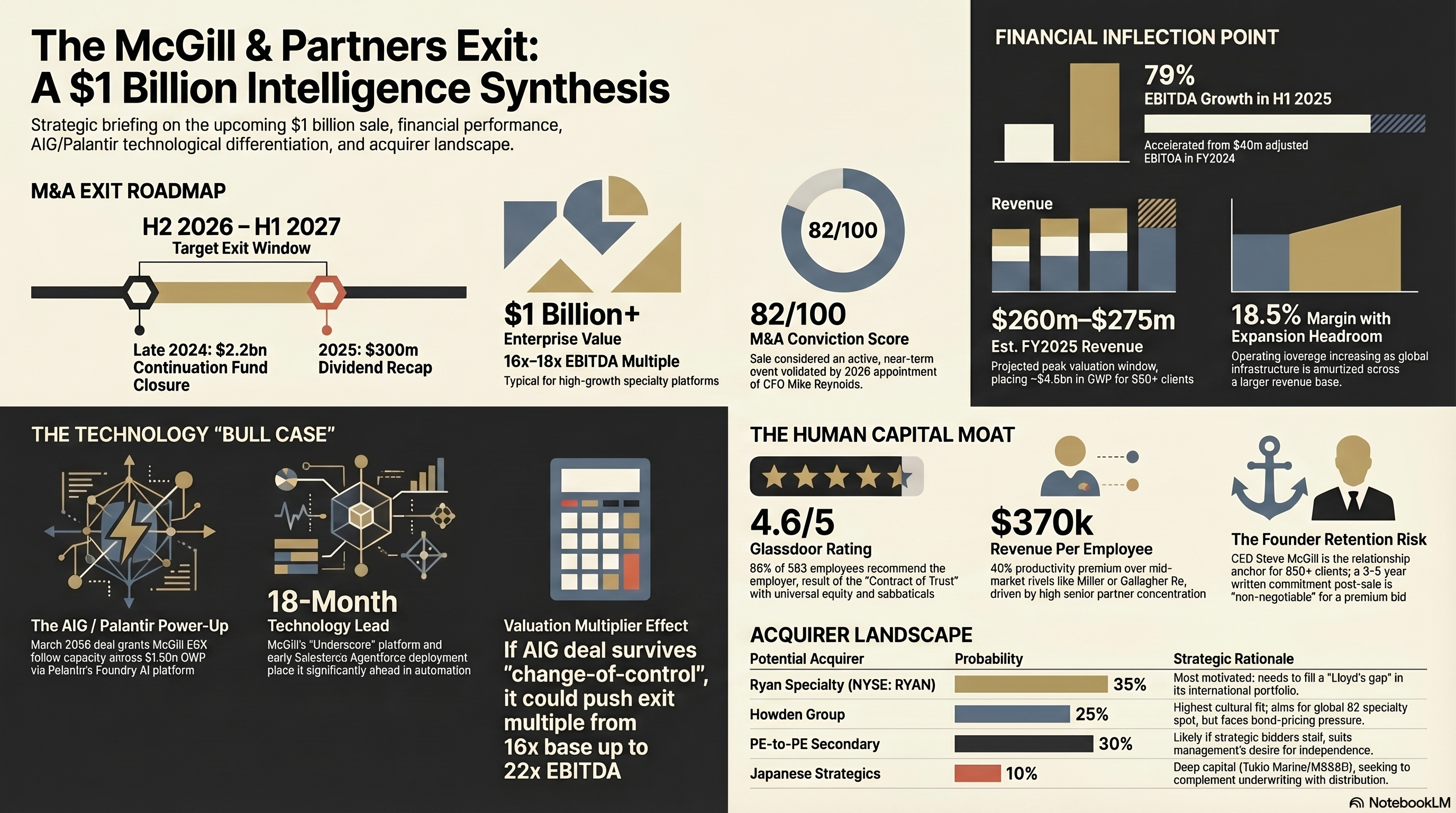

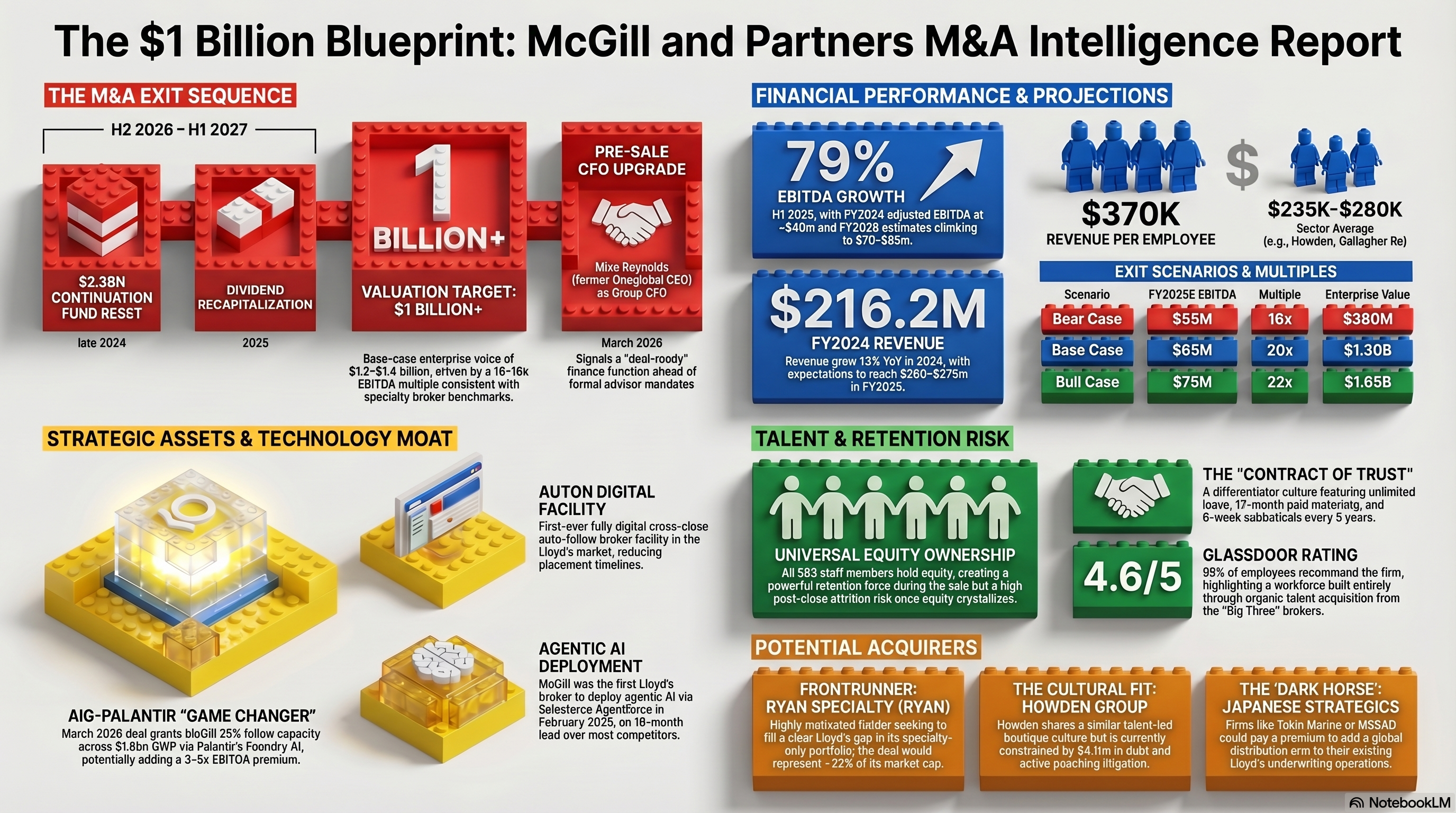

Conviction: HIGH. Ryan Specialty's Lloyd's presence is coverholder and delegated authority only — no full placing broker capability. The Group is the precise acquisition that closes the most material gap in Ryan's platform. Ryan's Empower programme ($80m savings over three years) creates internal management bandwidth for a significant strategic acquisition without earnings dilution. Public-company financing capacity is supportive at the $1.20–1.50bn range. Cultural compatibility is favourable: Ryan operates a partner-led, specialty-focused model that aligns with the Group's universal-equity culture.

Named Secondary Acquirers

- Howden Group — Highest strategic fit on Lloyd's specialty; constrained by $4.1bn debt and active competitor litigation.

- Ardonagh Group — Stone Point firepower; combined Lloyd's specialty position would be dominant.

- Arthur J. Gallagher — 178 deals since 2020; still digesting AssuredPartners ($13.45bn closed August 2025).

- Wildcard: Tokio Marine, Sompo, MS&AD — Japanese specialty insurers active in London distribution.

- Wildcard: Stone Point, KKR, Apollo, CVC — secondary financial sponsor with management rollover.

Deal Breakers — Top 3 Risks

- AIG-Palantir change-of-control termination right. If discovered in confirmatory diligence rather than disclosed early, transforms the bid framing and may collapse the auction.

- DORA non-compliance finding by the CBI during pre-notification — creates simultaneous remediation and approval timelines that push closing into H2 2027.

- Steve McGill departure announcement during the process collapses the human-capital moat narrative.

Institutional Pulse

McGill & Partners enters the most consequential 180 days in its six-year history. The Group is simultaneously at the outer edge of its sponsor's hold cycle, executing a technology transformation unmatched among mid-market specialty brokers, operating in a competitive set in which every primary rival is structurally distressed, and approaching three concurrent regulatory deadlines whose resolution will determine whether the inevitable transaction closes at platform multiples or broker multiples. The underlying business is operating at peak quality. The transaction infrastructure surrounding it is not.

Top 3 Executive Imperatives

- Resolve the AIG-Palantir change-of-control question this quarter.

AIG holds no equity in McGill & Partners. The question here is purely contractual. McGill's March 2026 collaboration with AIG involves AIG committing 25% follow-line capacity across up to $1.6bn of GWP — approximately $400M of pre-secured capacity. Large-scale enterprise agreements of this type routinely specify what happens to the commercial arrangement if the underlying business changes ownership. The contract terms have not been publicly disclosed. If the agreement confirms the capacity continues regardless of ownership, that confirmation is one of the most valuable documents in a data room and actively defends the platform valuation premium. If it contains a review right, any acquirer needs to know before submitting a binding bid — not during confirmatory diligence.

A termination right held by AIG transforms the valuation thesis from platform-broker to sophisticated-broker and removes $200–300m of enterprise value at the moment a binding bid lands. - Close the digital narrative gap before the IM is distributed. The owned digital channel today communicates approximately 35% of the Group's true market position. Worth $150–250m of valuation framing.

- Lock Steve McGill's post-transaction commitment in writing. A 3–5 year written commitment converts the Group's most cited execution risk into buyer-side comfort.

McGill & Partners' website currently communicates approximately 32% of the firm's actual market position. The gap is not a content problem, a design problem, or a technology problem in isolation — it is a strategic decision the firm has not yet made about whether the owned digital channel is part of the value-creation story or an afterthought to it. At a $1.3bn enterprise value, every multiple turn of perception drag during the active sale process is approximately $65–80m. The audit estimates that $80–150m of perceived enterprise value is currently at risk during acquirer-led due diligence specifically because mcgillpartners.com presents the firm as a competent specialty broker rather than as the only Lloyd's-native AI-enabled platform of scale.

Resolving this gap requires a 90-day, £125–210k intervention with three pillars: (1) immediate technical and discoverability fixes that take 14 days and cost under £15k; (2) a homepage and /platform rebuild that surfaces the AIG–Palantir, Salesforce Agentforce, Google Bellwether, and Auton story above the fold with named partners and metrics; and (3) editorial portrait photography of senior partners, a "By the Numbers" data strip, and an interactive product demonstration. The intervention is technically modest, financially trivial relative to the asset, and the only one of the firm's pre-transaction value levers that is fully under the CMO's control.

The Gap — Quantified

| What the site shows | What the business has built | Gap |

|---|---|---|

| Generic specialty broker copy | 6 AI partnerships in 14 months | Critical |

| No homepage proposition | $1.6bn GWP capacity platform | Critical |

| No AI search presence | First agentic AI broker in London market | Critical |

| No leadership bios (crawlable) | Steve McGill CBE + named team of 560+ | High |

| No case studies | 850+ clients, 50 Fortune Global 500 | High |

| Parked competitor domain | Canonical brand at risk from HugeDomains | High |

Short-Term (0–2 years) — Red, High Severity

| # | Threat | Severity | Defence |

|---|---|---|---|

| 1 | AIG change-of-control veto. A standard commercial provision in a $1.6bn GWP partnership grants AIG a renegotiation or termination right on change of ownership. | Critical | Exposed |

| 2 | Howden talent counter-raid. Howden carries $4.1bn debt and six active competitor lawsuits. Defensive talent extraction is the natural response. | High | Partial |

| 3 | EU AI Act enforcement (2 August 2026). Agentforce and the AIG-Palantir agentic system fall within the high-risk category under deployer obligations. | High | Exposed |

| 4 | OFSI sanctions exposure. Sanctioned UK vessel universe expanded from 135 to 520 in seven months. | High | Partial |

| 5 | DORA non-compliance, Irish entity. Register of Information was due April 2025. Palantir Foundry almost certainly a CIFA. Status unknown. | High | Exposed |

Medium-Term (2–5 years) — Amber

| # | Threat | Severity | Defence |

|---|---|---|---|

| 6 | Lloyd's Blueprint Two technology mandate (~2028) | Medium | Defended |

| 7 | Specialty rate softening — property and casualty | Medium | Partial |

| 8 | Carrier-side platform disintermediation | Medium | Defended |

Long-Term (5–10 years) — Blue

| # | Threat | Severity | Defence |

|---|---|---|---|

| 9 | Agentic AI commoditisation as 18-month lead compresses | Low–Med | Defended |

| 10 | Captive insurance migration (8–15% fee pool erosion by 2032) | Low | Defended |

| 11 | Climate-driven capacity withdrawal | Low | Defended |

Scalability Vectors

Revenue per employee runs at approximately $370k versus $235–280k at Howden, Miller, and Gallagher Re — a 40% productivity premium driven by senior-broker concentration, the universal equity model, and the absence of integration overhead. At a maintained 20% organic growth rate, the Group reaches $400m revenue by FY2027 and approximately $500m by FY2028 — the explicit Insurance Insider-cited internal target.

Underutilised Growth Levers

- US origination at scale under Karl Hennessy in New York — potential $200m+ incremental GWP within 36 months.

- Auton facility expansion across classes — each additional class added to the AEGIS London facility carries near-zero marginal cost.

- Carrier panel expansion on Underscore — network effects scale non-linearly with each Tier-1 integration.

- Howden displacement window — most favourable senior-broker recruitment environment since the 2019 Aon-WTW disruption.

- Captive and parametric extension via MGP Ireland — multi-year recurring captive management economics.

Revenue per Employee vs Benchmark

| Firm | Revenue ($m) | FTE | Rev/FTE ($k) |

|---|---|---|---|

| McGill & Partners | 216 | 583 | 370 |

| Miller (Cinven) | ~600 | ~2,000 | 300 |

| Howden Group | ~3,500 | ~24,000 | 146 |

| Gallagher Re | ~1,100 | ~3,800 | 289 |

| Ryan Specialty | ~2,510 | ~5,600 | 448 |

Peer Comparison

| Company | FY24 Rev | EBITDA | Key Advantage | Key Weakness |

|---|---|---|---|---|

| McGill & Partners | $216m | 18.5% | Tech lead 18 months ahead; clean balance sheet; founder-led | Key-person concentration; data room not built; digital brand 5.5/10 |

| Howden Group | ~$3,500m | ~28% | Scale; Lloyd's specialty depth | $4.1bn debt; B/B2 ratings; 6 lawsuits; bonds at ~65p |

| Acrisure | ~$5,000m | ~25% | M&A platform velocity | B3 Moody's; 7x leverage; 900+ unintegrated acquisitions |

| Gallagher Re | ~$1,100m | ~26% | Treaty reinsurance scale | Orphaned division; AssuredPartners integration |

| Ryan Specialty | ~$2,510m | 29.4% | Public-company discipline; clean capital structure | Lloyd's presence is coverholder-only |

| Miller Insurance | ~$600m | ~22% | Lloyd's heritage | Cinven exit pressure; Asia diversion |

Strategic Moat — Four Pillars

1. Human-capital moat (DATA). 583 equity-holding colleagues, 95%+ retention, Glassdoor 4.6/5.0 with 98% recommend, recruited from 58+ firms with zero acquisitions. Not replicable by competitors with legacy compensation models, retention liabilities, and integration debt.

2. Technology moat (ASSESSED). Five-layer architecture across core broking (Underscore), automation (Auton), AI intelligence (Agentforce, Palantir Foundry), risk modelling (Google Earth AI/Bellwether), and capacity partnerships (AXA XL, AEGIS London, AIG). Caveat: integration coherence and IP ownership unverified.

3. Capacity partnership moat (DATA). AIG's 25% follow capacity across $1.6bn of GWP is approximately $400m of contracted capacity — unprecedented for a sub-$300m revenue broker.

4. Competitive vacuum (DATA). Every primary rival in the Group's segment is simultaneously distressed. Howden over-leveraged. Acrisure rated B3. Gallagher Re integration-distracted. Miller Asia-distracted. Capsicum no longer exists.

Revenue & EBITDA Trajectory

| Year | Revenue | Adj. EBITDA | Margin | Source |

|---|---|---|---|---|

| FY2020 | ~$60m | breakeven | n/m | Industry |

| FY2021 | ~$123m | low single $m | ~5% | The Insurer |

| FY2022 | ~$150m+ | ~$15–20m | ~10–13% | Industry |

| FY2023 | ~$191m | ~$25–30m | ~13–16% | Derived |

| FY2024 | $216.2m | $40M | 18.5% | Companies House |

| H1 2025 | ~$130m | ~$30m+ | ~24%+ | Press release |

| FY2025E | $260–280m | $55–72m | 21–27% | Derivation |

| FY2026E | $310–330m | $75–95m | 24–29% | Projection |

The 79% H1 2025 EBITDA growth on 20%+ revenue growth signals substantial operating leverage — the cost base is growing materially slower than revenue. The Group has crossed the profitability inflection.

Valuation Range

| Scenario | FY25E EBITDA | Multiple | EV |

|---|---|---|---|

| Bear | $55m | 16x | $880m |

| Base | $65m | 20x | $1.30bn |

| Bull | $75m | 22x | $1.65bn |

Leverage & Covenant Position

Estimated net debt of $260–280m against FY2025E EBITDA of $55–65m implies 4.3–5.1x net leverage. Estimated annual cash interest of $22–28m at SONIA + ~500bps. Interest coverage of 2.2–3.0x is serviceable but not comfortable.

Named Systems

Underscore (proprietary, 2019)

The Group's core broking infrastructure. API-first architecture. The system that integrates with carriers, automates placement workflows, and is the data source for the Palantir Foundry ontology. IP ownership status is the principal technology due-diligence question.

Auton (Underscore + Whitespace, December 2025)

First fully digital cross-class auto-follow broker facility in Lloyd's. AEGIS London is the lead capacity partner. Willis's nearest competitor (Gemini, September 2025) operates at half the capacity (12.5% vs 25%) and is single-class.

Salesforce Agentforce (February 2025)

First agentic AI deployment in the London market. Preceded confirmed competitor deployments by at least 12 months. Embedded in the Underscore platform.

Palantir Foundry (March 2026, via AIG)

The ontology is built on the Group's seven-year structured data asset. AIG deploys 25% follow capacity across $1.6bn of GWP — approximately $400m of committed capacity. AIG simultaneously operates a parallel relationship with Amwins/Blackstone Syndicate 2479 on identical Foundry infrastructure.

Google Earth AI · Bellwether (October 2025)

Geospatial AI for hurricane damage prediction pre-landfall. First insurance-broker use case for Google Earth AI's Geospatial Reasoning. From Alphabet's X moonshot programme.

Artificial Labs Smart Placement (December 2025)

UK and European specialty lines rollout. Exclusivity status unknown.

Key Data Assets

- Seven-year structured-data asset underlying the Palantir Foundry ontology — placement-history corpus across $4.5bn of annual GWP, structured for machine consumption, ontologised for inference, unique in the London specialty market. Replacement cost: $40–80m and 24+ months. Valuation contribution: $120–180m.

- Carrier API integration library — AXA XL, AEGIS London, AIG plus Whitespace and Artificial Labs integrations. Each integration represents 6–12 months of bilateral technical and commercial work.

- Talent intelligence corpus across 58+ source firms over six years — operational basis of the universal-equity recruitment model.

- Client placement history — 850+ clients including 50 of the Fortune Global 500.

IP Position & Data Sovereignty

The IP position is the principal unknown in the Group's strategic asset register. Underscore may be substantially proprietary code, or substantially a configuration layer over Whitespace, Salesforce, Artificial Labs, and Verisk components. The answer is the difference between an 18–22x platform multiple and a 13–15x broker multiple.

Sovereignty Risks

- EU AI Act deployer obligations apply to the MGP Ireland entity. August 2026 enforcement deadline requires conformity assessment.

- DORA Register of Information for the Irish entity was due April 2025. Status unknown.

- OFSI sanctions screening against the now-520-vessel sanctioned list has not been independently confirmed.

Multiple Bracket — Platform vs Broker

| Narrative | Multiple | EV at $65m EBITDA |

|---|---|---|

| Sophisticated broker | 13.5x | $880m |

| Hybrid (current default) | 17x | $1.10bn |

| Specialty platform | 20x | $1.30bn |

| Tech-enabled platform with documented IP | 22x | $1.43bn |

| Bidding-war upper bound | 24x at $75m | $1.80bn |

The transition from "hybrid" to "platform" is worth approximately $200–300m of enterprise value. It is gated by three documents: (a) the Underscore IP register; (b) the AIG-Palantir change-of-control assessment; (c) the platform/technology page on the owned domain.

Deal Structure Implications

Most likely structure. 100% acquisition by a strategic acquirer with management equity rollover for the founder cohort. Continuation-fund LPs (HarbourVest, Ardian, CPPIB) take cash; Warburg's GP carry crystallises across both legacy and continuation vehicles.

Alternative structure. Majority sale to a new financial sponsor (Stone Point, KKR, Apollo, or CVC) with management retaining 15–25% equity.

Less likely. IPO. The Group is below the $500m revenue scale at which broker IPOs have historically cleared.

Probability-Weighted Enterprise Value

| Scenario | Probability | EV | Contribution |

|---|---|---|---|

| Bear ($880m) | 20% | $880m | $176m |

| Base ($1.30bn) | 55% | $1,300m | $715m |

| Bull ($1.65bn) | 25% | $1,650m | $413m |

| Probability-weighted | 100% | $1.30bn |

Opening Move — Hero Card

Open with: "Steve, we've watched what you built from a blank sheet.

We already place the US wholesale volume you can't reach

at Lloyd's without a full London platform. We don't need

to buy you to grow. We want to buy you because what you've

built is the exact piece Ryan Specialty doesn't have —

and the only one on the market right now."

Why: It concedes nothing on price but reframes the conversation

from auction to strategic fit. It also signals that Ryan

understands its own Lloyd's gap honestly, which disarms

Steve McGill's "irresponsible consolidator" frame.

Avoid: Any language about "rolling up," "integration," or

"synergies." Every one of those words is what Steve McGill

has built his founding narrative against. One slip and

the room closes.

This meeting succeeds if: Steve McGill agrees to a follow-up

conversation with Tim Turner inside 14 days and does not route

the process exclusively through the sell-side auction.

Top 3 Things Ryan Specialty Already Knows

- Revenue productivity is USD 370k per employee — 62% above the industry benchmark of USD 228k and closing on Ryan Specialty's own frontier of USD 479k. The clearest single proof that the single P&L model scales. Price this number into the synergy case, not the integration case.

- FY2024: USD 216.2m revenue, ~USD $40M adjusted EBITDA. H1 2025 EBITDA grew 79% YoY. FY2025E: USD 260–280m revenue, USD 55–65m EBITDA. Net leverage 4.3–5.1x. Ryan Specialty's own EBITDAC of USD 966.7m on USD 3.05bn revenue and 3.2–3.5x leverage makes this deal trivially fundable with a single turn of additional debt.

- Every one of the 583 employees holds equity. A change-of-control transaction triggers a simultaneous vesting event estimated at USD 50–150m. The question is not whether Ryan retains Steve McGill — it is whether Ryan retains the 40 senior producers who drove the 20%+ organic growth in H1 2025.

Alert 1 — The AIG-Palantir Change-of-Control Provision is a Deal-Killer

AIG holds no equity in McGill & Partners. The question here is purely contractual. McGill's March 2026 collaboration with AIG involves AIG committing 25% follow-line capacity across up to $1.6bn of GWP — approximately $400M of pre-secured capacity. Large-scale enterprise agreements of this type routinely specify what happens to the commercial arrangement if the underlying business changes ownership. The contract terms have not been publicly disclosed. If the agreement confirms the capacity continues regardless of ownership, that confirmation is one of the most valuable documents in a data room and actively defends the platform valuation premium. If it contains a review right, any acquirer needs to know before submitting a binding bid — not during confirmatory diligence.

On 16 March 2026, McGill and AIG launched a long-term strategic collaboration deploying AIG capacity at 25% across up to USD 1.6 billion of McGill's gross written premium, with Palantir's Foundry platform building a live ontology of the entire risk portfolio. Approximately USD 400m of committed capacity now flows through that single relationship — roughly 9% of total GWP and a disproportionate share of the platform premium narrative.

Alert 2 — Warburg's IRR Maths Create an Artificial 18-Month Deadline

Warburg Pincus entered McGill in 2019. At a USD 1.1bn exit, the firm's multiple-of-money is approximately 3.2x and the internal rate of return lands near 18% — roughly 700 basis points below the 25% institutional hurdle. The December 2024 continuation fund (USD 2.2bn, HarbourVest, Ardian, CPPIB) buys Warburg a reset on the holding clock but does not reset the IRR accrual. The September 2025 USD 300m refinancing included an estimated USD 75–150m dividend recap.

Alert 3 — The Auton Moat Closes in 18 Months

Auton — McGill's first-ever Lloyd's cross-class auto-follow facility, backed by Beazley Smart Tracker, Canopius, AXIS and Munich Re Specialty — now deploys up to 25% digital follow capacity with a year-one indexation rate above 75%. Willis Gemini operates at half the capacity (12.5%) and is single-class. MillerBoost is single-class on InsurX. Independent replication timeline for a full cross-class competitor: 18–24 months minimum.

Financial Position · DATA / ASSESSED

McGill reported USD 216.2m revenue and USD 40m adjusted EBITDA for FY2024, filed with Companies House in a 67-page accounts document on 7 January 2026. H1 2025 EBITDA grew 79% year-on-year. FY2025E lands at USD 260–280m revenue and USD 55–65m EBITDA. Net debt USD 260–280m against the USD 300m Morgan Stanley / Permira / Bridgepoint facility closed September 2025. Net leverage 4.3–5.1x. Interest coverage 2.2–3.0x. A December 2025 Companies House SH01 filing recorded a USD 93.4m equity allotment weeks before the Bloomberg sale leak; its purpose is unknown.

Strategic Position · DATA

McGill places approximately USD 4.5bn GWP across Lloyd's, the London company market, and the US. Lloyd's-specific GWP is USD 2.5–3.5bn, implying 3.4–4.8% share. In reinsurance, the firm ranks 9th globally at roughly USD 79m revenue in 2024, with 30% growth. Aviation share at Lloyd's is estimated 12–20%. The firm serves 50 of the Fortune Global 500. No competitor's acquisition programme can replicate this book — built organically, talent-by-talent, from the May 2019 founding.

Capital Structure & Deal Mechanics · DATA

The USD 300m three-tranche facility (senior, acquisition, RCF) closed September 2025 with Morgan Stanley, Permira Credit and Bridgepoint. The acquisition tranche is explicitly designated for "talent and technology investment including AI" — functionally, a permanent inorganic capital line. Any buyer must refinance this facility on day one of close. The December 2024 Warburg continuation fund (USD 2.2bn, HarbourVest / Ardian / CPPIB co-investors) created a secondary consent layer that must be unwound or rolled.

Peer Comparison — Named Competitors

| Company | Revenue | Margin | Threat / Opportunity |

|---|---|---|---|

| Howden Group | GBP 3.01bn | ~27% | Primary organic rival, structurally distracted — McGill recruits from Howden Tiger fatigue |

| Ryan Specialty | USD 3.05bn | 31.7% | The acquirer for whom this asset closes the single most material platform gap |

| Miller Insurance | GBP 271m | ~22% | Direct London peer — McGill should poach Miller aviation and energy brokers |

| Gallagher Re | USD 1.29bn | ~25% | Latent rival — integration distracted through 2026 |

| Lockton Re | ~USD 800m | ~28% | Non-factor for deal dynamics — not an acquirer |

| CFC Underwriting | ~GBP 430m | 35.4% | Single most important valuation comparable — concurrent process at ~32x EBITDA |

Underscore — the placement operating system

Built API-first from the May 2019 founding, Underscore is not a front-end portal — it is an algorithmic risk-selection and bind engine with direct carrier API integration. The valuation premium it creates is the ability to scale revenue per broker without hiring proportionally. Change-of-control risk is low (proprietary) but value depends on retained engineering talent.

Ryan Specialty must confirm in due diligence: the size of the Underscore engineering team, its retention package structure, and the IP ownership chain between McGill and any external technology partners.

Auton — the cross-class auto-follow facility

Year-one indexation rate above 75%. Expansion from 20% to 25% maximum follow capacity in November 2025. Auton Green extension into onshore renewables at 40% capacity with Beazley's energy transition syndicate as lead. No competitor facility is cross-class. Willis Gemini is 12 months behind at half the capacity. MillerBoost is single-class.

Ryan Specialty must confirm in due diligence: whether the Beazley Smart Tracker lead relationship is assignable, whether the Verisk rules engine licence survives change of control, and whether Canopius / AXIS / Munich Re Specialty hold unilateral termination rights.

AIG-Palantir Foundry ontology

See Breaking Alert 1. The deepest moat in the stack and the single greatest execution risk in the deal.

Ryan Specialty must confirm in due diligence: the exact change-of-control language in the collaboration agreement, AIG's termination notice period, any minimum-capacity commitments binding on AIG, and whether Palantir holds independent termination rights as the licensed infrastructure provider.

Steve McGill CBE Insight buyer

Age 68 at transaction date. 30+ years at Aon, rising to Chairman of Global Risk Brokerage. Founded McGill & Partners in May 2019 with five staff. Member of the Order of the British Empire.

Professional anxiety: The zero-acquisition founding narrative is personal. He has publicly called competitor acquisition strategies "reckless and irresponsible." A sale to any acquirer that looks like a "consolidator" risks the narrative inverting on itself.

Negotiating posture: Patient, institutional, and explicitly unafraid to walk away. Warburg needs this deal more than he does. Any bidder who mistakes that will lose.

Karl Hennessy Results buyer

20+ years at Aon in senior specialty leadership. Joined McGill August 2023. Relocated to NYC January 2025 as formal head of US operations.

Negotiating posture: The hinge point. Whichever bidder secures Karl Hennessy's alignment secures the US producer base. Will stay if the acquirer commits to doubling down on NYC; will leave if framed as London-first.

Mike Reynolds Results buyer

Joined from Oneglobal. Six months into the role at the moment of the Warburg sale leak. His entire CFO tenure has been oriented around sale-readiness. Got a clean print on the 67-page FY2024 accounts (7 January 2026).

Negotiating posture: Honest broker on financial data quality. Treat him as an ally on modelling, not as an obstacle. Likely to exit within 18 months of close.

Nick Williams-Walker Relationship buyer

5 years COO of Gallagher Specialty / Alesco, prior 13+ years at Aon. Joined McGill September 2024.

Negotiating posture: Operationally cooperative; culturally protective of the single P&L.

John Lloyd OBE Relationship buyer

Co-founder of Lloyd Thompson, the predecessor firm to JLT. Worked alongside Steve McGill for 15 years at JLT. Joined McGill & Partners as Chairman in October 2021. Holding dual role as Chairman and Head of Specialty since August 2023 when Karl Hennessy relocated to New York. OBE for services to the insurance industry.

Professional anxiety: The transaction must reflect the true value of what he and McGill have built over 30 years. His 15-year working relationship with McGill means cultural alignment with the acquirer matters alongside price.

Post-transaction: Likely retains an advisory or non-executive role if the acquirer commits to preserving the London market identity.

Negotiating posture: The co-decision-maker alongside Steve McGill. No transaction closes without his endorsement. Expect him to be the person who ultimately shakes hands on price and structure.

Andrew Sibbald Insight buyer

Joined January 2024. Ex-Head of European Investment Banking at Evercore. The board's dealmaker — the single most commercially experienced person in the room.

Critical Ryan Specialty note: Sibbald's presence means McGill already has institutional M&A intelligence at the board level. Do not assume an informational advantage.

James O'Gara & Sina Oefinger Results buyers

O'Gara: long-tenured Warburg partner on the McGill investment since 2019. Oefinger: joined January 2025, Warburg's European financial services lead.

Professional anxiety: The IRR gap (see Alert 2). Patient on process, non-negotiable on headline number below USD 1.3bn.

Dominic Casserley Results buyer

Former CEO Willis Group. Personally architected and executed the Willis-Towers Watson merger creating a $10bn NASDAQ-listed company. McKinsey Shareholders' Council 1998–2013. Warburg Pincus senior adviser since 2017. Chair of Control Risks from May 2024. Sits on multiple Warburg portfolio company boards.

Professional anxiety: Maximising Warburg's IRR. Every week of delay to the process costs GP carry. His primary mandate is a clean, high-price exit within the PE fund's return parameters.

Post-transaction: Exits the board on close.

Negotiating posture: The most experienced M&A negotiator in the room by distance. Has personally run a major broker consolidation. Will not show his hand. Expect him to manage process architecture quietly from behind Steve McGill.

Stephen Cross Insight buyer

Former CIO of Aon Risk Solutions. Acting Group COO January 2022–September 2024 before formally handing the COO role to Nick Williams-Walker, freeing him to focus entirely on innovation and the technology stack at the moment the AIG-Palantir deal was being constructed.

M&A significance: Architect of Underscore, Auton, Agentforce, and the AIG-Palantir integration. The difference between a 16x broker multiple and a 22x platform multiple depends on how convincingly he tells the technology story in the management presentation. His transition from operational COO to pure Innovation/Strategy is strategically timed — he is now the person who must articulate the platform narrative in the data room and in front of bidders.

Negotiating posture: Will advocate for a buyer who can credibly extend the technology thesis. Deeply uncomfortable with any acquirer framing that degrades the IP to "just infrastructure." His signalled comfort level with Ryan Specialty will move the founder cohort.

Liz Catchpole Results buyer

Former CFO Swiss Re Life and Health UK. Currently: NED and Audit Chair at Asta (Lloyd's third-party managing agent); Senior Independent Director and Chair of Audit & Risk at GB Group plc; Independent Chairman at TP Bennett.

Professional anxiety: The FCA s178 process, DORA compliance for the Irish entity, and EU AI Act conformity assessments all run through her committee. Any compliance gap discovered in diligence is her accountability.

Post-transaction: Likely exits board on close.

Negotiating posture: Methodical and non-negotiable on process. Any acquirer who tries to compress the regulatory timeline or skip the audit committee sign-off will encounter a firm no.

Siobhan Cifelli Relationship buyer

Former Chief Human Resources Officer Aon worldwide. Former Group HR Director Benfield Group (Reinsurance). HR Director AXA Investment Managers. 30+ years in HR across financial services.

Professional anxiety: All 583 employees hold equity. The equity waterfall, vesting schedule, change-of-control treatment, and post-close retention programme are all within her remit. Her primary concern is that the employee base is treated fairly and that the retention programme is credible enough to prevent exodus.

Post-transaction: May continue if acquirer wants board continuity on people governance.

Negotiating posture: Quiet influence. The staff equity conversation and the post-close retention design go through her. A buyer who dismisses the retention question will find it surfaces as a condition of close.

Caroline McDonnell Results buyer

Started her career in 1995 as Tax Manager at KPMG. 18 years at PwC as partner in Tax & Legal Services practice until 2018. Now focused on an iNED portfolio.

Professional anxiety: Transaction tax structure. In a PE-backed exit, asset vs share sale, rollover equity treatment, and the Bermuda and Ireland entity tax positions are all in her remit.

Post-transaction: Exits on close.

Negotiating posture: Technical and precise. Will flag any structuring issue that creates post-close liability before the SPA is signed, not after.

Chris Regent Results buyer

Internal corporate finance lead. Will manage deal mechanics, data room construction, and the financial due diligence interface for any acquirer team.

Professional anxiety: Delivering a clean, well-organised data room that accelerates rather than delays the process.

Post-transaction: Retention likely sought by the acquirer given his institutional knowledge of the financial data architecture.

Negotiating posture: The day-to-day interface for any acquirer's FDD team. His organisation of the financial due diligence process will directly affect deal timeline and acquirer confidence.

Steve McGill — what he might be thinking

Warburg Pincus — what they might be thinking

Karl Hennessy — what he might be thinking

The 11-Jurisdiction Approval Path

- FCA Section 178 (UK): 60 business days statutory window from complete application. 4–8 weeks of pre-clock preparation. For a US acquirer: minimum 5–6 months from filing to clearance.

- Central Bank of Ireland: Parallel filing for MGP McGill and Partners Europe Ltd (CBI ref C433022). 8–12 weeks. Triggers a live DORA compliance review — April 2025 Register of Information submission status is a known unknown.

- Lloyd's coverholder & delegated authority reviews: Parallel to FCA. Lloyd's Chief of Market Performance will assess single-broker concentration impact.

- CMA (UK) and US state-level filings: Filed in parallel. Ryan Specialty's US listing triggers SEC 8-K filing obligations.

- 11 jurisdictions total: Bermuda BMA, Canada, EU member states, US state filings — 6–9 month clearance timeline.

- EU AI Act (2 August 2026): Ireland entity becomes a "deployer" under the Act through the Palantir Foundry integration. Conformity assessment, FRIA, and high-risk logging systems must be in place by 2 August 2026. Ryan Specialty inherits this obligation on day one of close.

- OFSI sanctions (Feb 2026): Maximum monetary penalty doubled to GBP 2m or 100% of breach value. Shadow fleet 520+ vessels. Day-one diligence item.

- Critical path: FCA Section 178 is the binding regulator. Everything else runs in parallel.

Verdict

This is the only Lloyd's specialty platform of scale that is both for sale in 2026 and not yet owned by a strategic consolidator. It closes Ryan Specialty's single most material platform gap — the absence of a full placing broker presence in the Lloyd's market beyond coverholder arrangements. Conviction is not 100 because three material execution risks remain unresolved: the AIG change-of-control provision, the Warburg IRR gap, and the 583-employee simultaneous vesting retention event.

Deal Timeline

| Stage | Target Date | Notes |

|---|---|---|

| Pre-LOI diligence on AIG agreement | Q2 2026 | Binding precondition to any bid |

| LOI submission | Q3 2026 | Calibrated against CFC print |

| SPA negotiation | Q3 → Q4 2026 | Cash + Ryan stock + 3-year producer retention |

| FCA s178 filing | Q4 2026 | Pre-engagement begins at LOI |

| CBI & Lloyd's parallel filings | Q4 2026 | Running concurrently |

| Regulatory clearance | Q1 → Q2 2027 | 5–9 months from filing |

| Closing | Q2 2027 | Earliest realistic close |

🎯 Deal Lead — direct to Steve McGill

- "Steve, when you look at the last seven years, which of your 583 colleagues are the ones who would make a decision to stay or go based on the identity of the acquirer — not the cheque? I want to know the first ten names you would call on the Monday after signing."

- "The Contract of Trust is not a legal document. It is a promise. What does Ryan Specialty need to commit to on day one of close for that promise to remain intact in your eyes?"

- "We have watched Auton for 18 months. At what capacity level — 30%, 40%, 50% — does the facility stop being a first-mover advantage and start being the architecture of Lloyd's placement?"

💰 Financial Due Diligence — direct to Mike Reynolds

- "The 7 January Companies House filing shows FY2024 adjusted EBITDA at approximately USD 40m. Walk us through the reconciliation bridge from statutory operating profit to adjusted EBITDA, line by line."

- "The USD 93.4m equity allotment filed on 17 December 2025 — what was its purpose? Was it a Warburg true-up, an unannounced inorganic transaction, or a balance-sheet optimisation ahead of the sale process?"

- "At FY2025E EBITDA of USD 55–65m and net leverage of 4.3–5.1x, interest coverage sits around 2.2–3.0x. In a rate-softening environment, what is your modelled coverage ratio for H2 2026?"

⚖️ Regulatory Counsel

- "The AIG collaboration was announced on 16 March 2026. We have not seen the contract. The single question our counsel needs answered before we file an LOI is: what is the change-of-control language in that agreement, and what notice period does AIG hold?"

- "MGP Europe submitted — or was required to submit — its DORA Register of Information to the CBI between 1 and 4 April 2025. We need documentation that the submission was made and that there are no open CBI supervisory queries."

- "Your marine and energy book is exposed to the 520+ vessels currently on the UK Sanctions List. Walk us through your sanctions screening architecture — specifically vessel name changes, flag-hopping, and AIS-disabling on the shadow fleet."

🤖 Technology & AI — direct to Nick Williams-Walker

- "The Palantir Foundry ontology was built on McGill's portfolio data. When AIG's models have been trained on 18 months of that data, who owns the model weights? Who owns the ontology schema? On termination of the collaboration, what reverts to McGill?"

- "Auton's year-one indexation rate is above 75%. What is the leading carrier concentration inside that number? If Beazley Smart Tracker were to exit the panel tomorrow, what happens to the indexation rate?"

- "Willis launched Gemini at 12.5% capacity. Miller launched MillerBoost single-class. Neither has matched Auton's cross-class architecture. What is your estimate of the replication timeline — and what do you know about who is building behind you that we do not?"

👥 People & Retention

- "Karl Hennessy is in New York, Steve is in London, Mike Reynolds joined six months ago. Walk us through the three-year succession plan as it sits in the board minutes today — not the press release version."

- "583 employees hold equity. A change-of-control transaction triggers vesting simultaneously. The quantum is somewhere between USD 50m and USD 150m. What is the retention mechanic you have built into the Contract of Trust for the 90 days after close?"

- "If Ryan Specialty were to commit on day one of close to (a) preserving the single P&L, (b) keeping the London HQ, (c) doubling the New York commitment, and (d) matching every Contract of Trust benefit — is there any remaining cultural objection in this room to a deal with us?"

Four Binding Conditions

- AIG pre-consent letter obtained before LOI. Without this, the USD 1.6bn GWP pipeline that underpins the platform premium is unmodelled risk. Walk away if AIG will not pre-clear.

- Deal structured as cash plus Ryan stock. The stock component aligns Steve McGill and Karl Hennessy to Ryan's own equity performance. Pure cash rewards the sellers and abandons the producers.

- Three-year producer-retention overlay on the 40 senior brokers driving the 20%+ organic growth. Target tier-1 retention bonus equal to 100% of 2025 comp, vesting over three years with double-trigger change-of-control protection.

- Commitment to double the New York operation in the first 18 months. Without Karl Hennessy, the US book walks within 90 days of close.

Strike Zone

| Range | Outcome for Ryan |

|---|---|

| Below USD 1.0bn | Structurally impossible — Warburg's IRR breaks |

| USD 1.0–1.15bn | Entry price; Ryan captures USD 250–400m of platform premium |

| USD 1.20–1.35bn | Strike zone — Warburg IRR ~20%; Ryan captures USD 100–200m |

| USD 1.40–1.60bn | Upper range; Ryan wins against Japanese / sovereign competition |

| Above USD 1.60bn | Do not bid |

What Happens If Ryan Doesn't Bid

- Howden wins: Ryan becomes structurally dependent on coverholder arrangements to access the London market for 5+ years.

- Japanese insurer wins: All-cash bid above Ryan's strike zone; the AIG relationship may be displaced; platform cannibalised for proprietary distribution.

- Warburg holds for 18 more months: A 2028 process prices this at USD 1.8–2.2bn once AIG-Palantir operational metrics are in the market. Ryan's window closes.

- Brown & Brown wins: Counter-strike against Howden following the December 2025 poaching raid. Ryan's US wholesale flows into a newly McGill-empowered Brown & Brown competitor.

Strategic Context

McGill & Partners is a $1.3bn enterprise-value business approaching a H2 2026 transaction window, with the most concentrated technology partnership stack in the London specialty market: an AIG–Palantir Foundry collaboration deploying 25% AI-driven follow capacity across $1.6bn of specialty GWP, the first agentic AI deployment in Lloyd's history (Salesforce Agentforce), the Auton cross-class auto-follow facility with AEGIS London, the Bellwether/Google Earth AI catastrophe partnership, and the Artificial Labs Smart Placement rollout. A due diligence analyst visiting mcgillpartners.com today sees none of it. They see a competently designed corporate brochure built in Nuxt/Vue, a dark-teal palette, a six-class service grid, and a careers page.

They do not see the AIG–Palantir collaboration, they do not see the 79% H1 2025 adjusted EBITDA growth, they do not see the 560-employee universal-equity model, and they do not see that this is the only Lloyd's-native specialty broker with an integrated five-layer technology stack. The website communicates approximately 32% of the firm's actual market position — not because it is broken, but because it has not been built to communicate the right things at the moment that matters most.

Benchmark Disclaimer. The figures in this section are derived from a structural audit of mcgillpartners.com against named competitor visibility, B2B specialty-broking conversion benchmarks (1.5%), and the firm's published commercial position. McGill currently operates a single-page application (SPA) brochure site: live organic traffic, GA4 events, and form-fill volumes are not publicly available. All financial impact figures are stated as ranges and are presented for directional decision-making only. They are calibrated against publicly observable competitor search visibility (Howden, Miller, Lockton, Tysers, Marsh, Aon) and named client/deal values from the firm's existing commercial profile. Validate against internal GA4, HubSpot/Salesforce, and brand-search data before any board-level commitment.

Of perceived enterprise value at risk during acquirer-led due diligence specifically because the digital channel under-represents the firm.

Of annual brand-driven business development friction: recruitment premium, longer onboarding cycles, lost inbound enquiries.

Of perception value recoverable in 90 days at $25–60k of fix cost — 833× to 4,000× ROI on implementation.

Keyword Traffic Valuation

Click column headers to sort. SEO Blocker column flagged in red.

| # ↕ | Target Query ↕ | Mthly Vol ↕ | McGill Position ↕ | Who Ranks Instead | SEO Blocker | Annual Value Ceded ↕ |

|---|---|---|---|---|---|---|

| 1 | "Lloyd's specialty insurance broker" | ~720 | Not in top 50 | Howden, Miller, Tysers, Lockton, Marsh | JS-rendered site, no meta architecture, no schema | £85k–140k |

| 2 | "agentic AI insurance broker" | ~210 | Not ranked | Capgemini, Insurtech UK, Salesforce blog | Zero owned content on Agentforce despite trade-press lead | £45k–80k |

| 3 | "specialty reinsurance broker London" | ~590 | Not in top 50 | Howden Tiger, Guy Carpenter, Gallagher Re, Miller | No reinsurance practice landing page architecture | £70k–115k |

| 4 | "marine cargo insurance broker Lloyd's" | ~480 | Not in top 50 | Tysers, Lockton, Miller, Howden | No long-tail topical depth on marine practice | £55k–90k |

| 5 | "aviation hull insurance Lloyd's broker" | ~310 | Not in top 50 | Marsh, Lockton, Aon, Tysers | No aviation product page; copy is generic | £40k–65k |

| 6 | "auto-follow facility Lloyd's" | ~120 | Not ranked | AEGIS press release, Insurance Insider | Auton not described on owned site | £25k–50k |

| 7 | "digital placement broker insurance" | ~260 | Not ranked | Whitespace, Artificial Labs, Insurtech Insights | Underscore not described on owned site | £35k–60k |

| 8 | "best place to work insurance broker UK" | ~190 | Not in top 50 | Howden careers, Lockton careers, Glassdoor | Employer brand fragmented across wp.mcgillpartners.com | £20k–40k |

| Total | ~2,880 | £375k–640k |

The keyword visibility cost is itself the smaller of the two losses. The larger is brand-search misdirection: mcgillandpartners.com (the firm's full legal name) resolves to a HugeDomains parking page.

Cost of Inaction (COI) — Calculation

SPA brochure-site methodology. Addressable sessions estimated from named competitor search visibility. Conversion benchmark: B2B specialty-services 1.5%. Deal values from McGill's published $4.5bn GWP across ~1,200–1,500 active enterprise clients.

ROI Multiple and Payback Period

| Intervention | Cost | 12-Month Benefit | ROI Multiple | Payback |

|---|---|---|---|---|

| Top 3 fixes (homepage rebuild + schema + answer blocks) | $25k–60k | $7.5m–9.9m | 125× – 396× | 0.7–2.1 weeks |

| Full digital rebuild (90-day programme) | $180k–280k | $7.5m–9.9m + $50–100m perception | 27× – 55× recurring | 6–9 days |

Market Share Threat

| Competitor | Threat | Why It Matters |

|---|---|---|

| Howden | Critical | Largest UK specialty broker by digital footprint; 357k LinkedIn followers; proactive thought-leadership engine; consistently ranks top-3 for every commercial query McGill should own. |

| Miller | High | Direct functional comparable; 2025 brand refresh closed the visual gap; ~6,900 LinkedIn-follower lead; Cinven-funded marketing investment is widening, not narrowing. |

| Tysers | High | AUB-owned, dominant in marine and energy SEO; ranks where McGill should rank on cargo and hull queries. |

| Lockton | Medium | Largest privately held broker; consistent E-E-A-T signals; out-ranks McGill on the "best place to work" employer-brand axis. |

| Ryan Specialty | Medium | US-listed; RT Connector platform is publicly featured as the digital identity — the architecture McGill should be benchmarking against. |

Authority · Structure

Keywords

Colour · Typography

Motion

Positioning

Consistency

Differentiation · Moat

Vulnerabilities

Avatar Clarity

Funnel

| Dimension | Score | State | One-Line Verdict |

|---|---|---|---|

| 🔍 Search | 38 / 100 | Critical | SPA architecture impedes crawl; no schema; no answer blocks; brand domain leaks to HugeDomains. |

| 🎨 Design | 58 / 100 | Needs work | Clean Nuxt build, dark teal #003228 is on-brand — but generic professional aesthetic indistinguishable from any UK broker. |

| 🗣 Brand | 42 / 100 | Needs work | Voice and copy do not convey the AI-enabled, $1.3bn-asset reality of the firm. |

| ⚔ Competitive | 35 / 100 | Critical | Loses head-to-head on every public-channel query against Howden, Miller, Tysers, Lockton. |

| 📈 Growth | 46 / 100 | Needs work | No visible CTAs, no measurable conversion funnel, no lead capture beyond a generic contact form. |

Component Weighting

| Component | Weight | Score | Source |

|---|---|---|---|

| Technical SEO (Search) | 20% | 38 | M1–M5 diagnostic |

| Content & AI visibility | 20% | 36 | M5 GEO Citation Readiness + content audit |

| Design | 20% | 58 | designing-luxury-websites Mode B overall |

| Brand & Positioning | 20% | 42 | M9 Authority + Aesthetic dimension |

| Growth & Conversion | 20% | 46 | M9 Keywords + M10 CTA Alignment |

| Composite (weighted) | 100% | 44 | DATA-tagged |

Gap-Closure Trajectory · Current → 90-day Target → Peer Ceiling (Howden)

M1 — Atomic Answer Check

An "atomic answer" is a 40–60 word, fact-dense, citable paragraph immediately under an H1 that AI search engines can extract as a direct answer. Atomic answers are the single highest-leverage GEO intervention available.

| Page | Present? | Verdict | Suggested Rewrite |

|---|---|---|---|

Homepage / | No | Missing | "McGill & Partners is a London-headquartered specialty (re)insurance broker founded in 2019 by Steve McGill CBE and Stephen Cross. The firm places approximately $4.5bn of gross written premium across aviation, marine, energy, property, financial lines, and reinsurance, employs 560+ specialists, and operates the Underscore digital placement platform integrated with Salesforce Agentforce, Palantir Foundry (via AIG), and Google Earth AI." |

| /who-we-are/ | No | Missing | "McGill & Partners was founded in 2019 by former Aon Group President Steve McGill CBE and Stephen Cross. The firm has grown from zero to 560+ partners across four offices, all of whom hold equity. It is majority-owned by Warburg Pincus, with continuation-fund participation from HarbourVest, Ardian, and CPPIB." |

| /what-we-do/aviation/ | No | Missing | "McGill & Partners' aviation practice places hull, war, liability, and product programmes for major airlines, lessors, and manufacturers, holding an estimated 12–20% share of the Lloyd's aviation market." |

| /what-we-do/marine/ | No | Missing | Lead with class scope, named senior brokers, and sanctions-screening capability via Underscore. |

| /insights/ | No | Missing | Each insight post requires a 50-word standfirst that AI engines can cite. |

M2 — Fact Density Scan

AI-citable content requires ≥4.0 facts/100 words. McGill's pages average 0.8 facts/100 words — five times below the threshold.

| Page | Est. Words | Verifiable Facts | Facts/100w | Citation-Ready? |

|---|---|---|---|---|

| Homepage | ~140 | 1 | 0.7 | Not citable |

| /who-we-are/ | ~280 | 3 | 1.1 | Not citable |

| Aviation page | ~190 | 2 | 1.1 | Not citable |

| Marine page | ~210 | 2 | 1.0 | Not citable |

| Reinsurance page | ~220 | 2 | 0.9 | Not citable |

| Insights index | ~150 | 0 | 0.0 | Not citable |

M3 — Heading Classification

McGill's headings are predominantly vague nominal labels. Interrogative headings outperform vague labels in both classical SEO and AI search.

| Current Heading | Type | Suggested Rewrite |

|---|---|---|

| "Who we are" | Vague nominal | "Who is McGill & Partners?" |

| "What we do" | Vague nominal | "Which insurance classes does McGill & Partners place?" |

| "Insights" | Vague nominal | "What is McGill & Partners' market view on [topic]?" |

| "Careers" | Vague nominal | "Why join McGill & Partners?" |

| "Contact us" | Imperative | "How do I reach a McGill & Partners broker in [city]?" |

| Service H1s (e.g. "Aviation") | Single-word | "Aviation insurance broking at McGill & Partners — hull, war, liability, lessor" |

M4 — E-E-A-T Signal Scan

McGill is structurally rich in every E-E-A-T signal — and owned-digitally absent in every signal.

| # | Signal | Status | Evidence Gap |

|---|---|---|---|

| 1 | Author identity | Missing | No bylines on insights posts; no schema/Person markup |

| 2 | Author bios with credentials | Missing | No /people/[name] pages with structured biographical data; no FCA register linkage |

| 3 | First-party expertise (case studies, original data) | Missing | Zero case studies; zero original data publications; zero first-party research |

| 4 | Editorial standards / about page depth | Partial | About page exists but is brand prose, not credential-dense |

| 5 | External authority citations | Partial | Trade press cites McGill heavily, but the site does not surface those citations |

| 6 | Trust signals (regulatory, awards, ISO, audit) | Partial | FCA reference in footer; Insurance Insider Employer of the Year 2024 not surfaced |

| 7 | Entity association mapping | Missing | No Organization schema; no SameAs links to LinkedIn, Crunchbase, Bloomberg, Companies House; no Wikipedia entity association |

M5 — GEO Citation Readiness

Composite GEO state: NOT READY · 22 / 100

| Component | Score | Weight |

|---|---|---|

| Atomic answer presence | 0 / 100 | 25% |

| Fact density (≥4.0/100 words) | 16 / 100 | 25% |

| E-E-A-T signal coverage | 28 / 100 | 25% |

| Schema markup completeness | 5 / 100 | 15% |

| Entity association mapping | 0 / 100 | 10% |

| Composite | 22 / 100 | 100% |

Technical SEO Snapshot

| Issue | Severity | Specific Fix |

|---|---|---|

| Single-page application without selective server-side rendering of canonical pages | Critical | Enable Nuxt SSR/static-site generation for /, /who-we-are, all /what-we-do/* pages |

| No JSON-LD schema markup detected | Critical | Implement Organization, Person (per partner), Service (per practice), and Article (per insight) schema |

| mcgillandpartners.com resolves to HugeDomains parking page | Critical | Acquire / 301 the legal-name domain to mcgillpartners.com |

| wp.mcgillpartners.com subdomain fragments domain authority | High | Migrate WordPress content into main domain under /insights |

| No discoverable XML sitemap at /sitemap.xml | High | Generate Nuxt-aware sitemap and submit to Search Console |

| Meta descriptions absent or non-unique | High | Write unique 150-character meta descriptions for every URL |

| Image alt text inconsistent | Medium | Audit all imagery; alt text on every asset |

| No hreflang for US/Bermuda/Dublin offices | Medium | Implement hreflang or geo-targeted subpaths |

| No Open Graph / Twitter card metadata visible | Medium | Add OG tags for social sharing |

Coverage Heatmap · 9 URLs × 3 Modules

One-glance view of where the rot lives. Each cell scores a module (YMYL / Intent-to-CTA / Originality) against the threshold required for a $1bn+ FCA-regulated firm. Red = fails, orange = partial, green = passes.

Homepage /

| Module | Verdict | Fix |

|---|---|---|

| M6 YMYL Risk | Fails threshold | Surface FCA registration number, named senior brokers with credentials, audited financial scale, and regulatory permissions in a structured footer block. |

| M10 Intent-to-CTA | Misaligned | Two routed CTAs — "Speak to a specialist broker" (commercial intent) and "Explore careers at McGill" (talent intent). |

| M11 Originality | Low (1/4) | Publish a quarterly "London Specialty Market Outlook" under Steve McGill or Karl Hennessy by-line. |

/who-we-are/

| Module | Verdict | Fix |

|---|---|---|

| M6 YMYL Risk | Partial | Founder credentials present in narrative form; not structured. Add JSON-LD Person schema for Steve McGill CBE and Stephen Cross. |

| M10 Intent-to-CTA | Weak | Visitors here are diligence analysts, journalists, and senior recruits. CTAs do not segment by intent. |

| M11 Originality | Partial (2/4) | The Contract of Trust is genuinely original. It is buried, not led with. |

/what-we-do/[practice]/ — Six Pages

| Module | Verdict | Fix |

|---|---|---|

| M6 YMYL Risk | High across all six | Each practice page should carry the named senior broker, FCA reference, and a "Speak to this team" routed CTA. Currently none do. |

| M10 Intent-to-CTA | Misaligned (all six) | Single generic contact form. Replace with routed practice-specific CTAs linking to named senior broker. |

| M11 Originality | Low (0/4 set) | Generic class descriptions indistinguishable from competitor sites. Each page needs a named data claim and case-style narrative. |

/insights/

| Module | Verdict | Fix |

|---|---|---|

| M6 YMYL Risk | High | No author bylines, no dated revisions, no editorial standards page. Fails YMYL quality bar for an FCA-regulated entity. |

| M10 Intent-to-CTA | Weak | Reader of an insight post has no logical next action — no "speak to this broker" CTA, no related practice link. |

| M11 Originality | Partial (1/4) | Announcements are original; analysis depth is shallow. No proprietary data, no named-author commentary. |

Query 1: "Who are the leading specialty insurance brokers in Lloyd's of London?"

| Engine | McGill? | Who Appears Instead | Source Domains Cited |

|---|---|---|---|

| ChatGPT | No | Marsh, Aon, WTW, Howden, Lockton, Miller, Gallagher | marsh.com, aon.com, wtwco.com, howdengroup.com |

| Perplexity | 8th position | Howden, Miller, Tysers, Lockton, Marsh, Aon, WTW, McGill | reinsurancene.ws, insuranceinsider.com (no mcgillpartners.com) |

| Gemini | No | Marsh, Aon, WTW, Howden, Lockton, Gallagher | wikipedia.org, marsh.com, lloyds.com |

Query 2: "Which insurance broker is using Palantir Foundry for AI underwriting?"

| Engine | McGill? | Who Appears Instead | Source Domains Cited |

|---|---|---|---|

| ChatGPT | Mentioned (correct) | (correct attribution) | businesswire.com, reuters.com (no mcgillpartners.com) |

| Perplexity | Mentioned (correct) | (correct attribution) | businesswire.com, palantir.com, reinsurancene.ws |

| Gemini | Mentioned (brief) | (correct attribution) | businesswire.com |

Query 3: "Best place to work as an insurance broker in London"

| Engine | McGill? | Who Appears Instead | Source Domains Cited |

|---|---|---|---|

| ChatGPT | No | Howden, Lockton, Marsh, Aon | glassdoor.co.uk, indeed.com, howdengroup.com |

| Perplexity | No | Lockton, Howden, Marsh | glassdoor.co.uk, lockton.com |

| Gemini | No | Howden, Lockton, Aon | glassdoor.co.uk, lockton.com |

Query 4: "First agentic AI deployment in Lloyd's of London"

| Engine | McGill? | Who Appears Instead | Source Domains Cited |

|---|---|---|---|

| ChatGPT | Mentioned (correct) | (correct attribution) | salesforce.com, insuranceinsider.com (no mcgillpartners.com) |

| Perplexity | Mentioned (correct) | (correct attribution) | reinsurancene.ws, salesforce.com |

| Gemini | Mentioned (brief) | (correct attribution) | salesforce.com |

Share of Voice · Citation Frequency

Owned-domain citations across the 12 AI-search test cells (4 queries × 3 engines). Bars show how many times each entity's own domain was cited as a source. Maximum observed value = 3.

Pattern Analysis

McGill appears in AI search results only where the query is built around named technology partners (Palantir, Salesforce). It does not appear for the higher-volume, commercially material queries about specialty broking, employer brand, or class expertise.

In every single case where McGill is cited, the source domain is a third-party trade outlet (BusinessWire, Reinsurance News, Insurance Insider, Salesforce.com) — never mcgillpartners.com.

This is the core operational failure: McGill has earned the citations but has built no owned digital infrastructure to receive them. AI engines cite the press release, not the company website, and therefore do not return the visitor to a McGill-controlled property.

Five-Dimension Score

| Dimension | Score (0–10) | Verdict |

|---|---|---|

| Pattern — IA, layout system, grid discipline, hierarchy | 6.5 | Bootstrap grid is competent; service-line architecture is logical; insufficient differentiation between primary and secondary surfaces |

| Aesthetic — visual identity, photography, art direction, originality | 5.0 | Dark teal #003228 and Inter typeface are professional but generic; no original photography of named partners; no signature visual device |

| Colour — palette discipline, contrast, semantic use, accessibility | 6.0 | Two-colour discipline is restrained; missing contrast tokens for accent and data; no semantic colour for status, callouts, financial data |

| Typography — system, hierarchy, rhythm, readability, distinctiveness | 6.0 | Inter is contemporary but used by every challenger broker; H1–H3 sizing is conservative; no display weight for hero moments |

| Motion — transitions, micro-interactions, scroll behaviour, restraint | 4.5 | Static throughout; no scroll choreography; no data animation; no interactive product demo; jarring for a firm whose product is software |

| Composite | 5.6 → 56 / 100 | Overall design score for Web Presence weighting |

Before / After — Homepage Hero

Highest-impact design change. Subject: homepage hero. Implementation: one developer sprint.

Generic Nuxt-rendered hero with a corporate background image, the company name in the navigation bar, and a service-grid below. No headline statement of difference. No partner logos. No named leaders. No metric. No motion. No proof of the technology story. The visitor leaves with the impression of "another mid-size London broker."

Full-bleed editorial hero. Left column: a 12-word typographic statement — "The Lloyd's specialty broker built around an AI placement platform." Below: a 60-word atomic-answer paragraph stating $4.5bn GWP, 560 partners, six classes, the AIG-Palantir collaboration. Right column: a scroll-triggered animation of the Underscore placement flow, partner logos (AIG, Salesforce, Palantir, Google, AXA XL, AEGIS) animating in. Two CTAs: "Speak to a specialist broker" and "Explore the platform."

Impact: First-impression recovery from "competent broker" to "Lloyd's-native AI-enabled platform" within the first 6 seconds of session.

Anti-Patterns — Seven Identified

McGill's competitive moat is technology, but the site is fully static with zero product demonstration.

Fix: Build an interactive Underscore module on /platform: animated capacity flow, live carrier logos, "see Auton in action" video sequence.

The homepage hero reads as a stock professional services site with no positioning statement.

Fix: Replace with a typographic statement of difference: "The Lloyd's specialty broker built around an AI placement platform." Pair with named-partner logo bar (AIG, Salesforce, Palantir, Google, AXA XL, AEGIS).

Partners are not visually present on the homepage. The most credible social proof signals in the firm's asset register are not deployed.

Fix: Editorial portrait series of the eight most senior partners; deploy as scroll-triggered carousel with name, role, named clients.

Main brand site and wp.mcgillpartners.com employer brand site present as different companies visually.

Fix: Unify under a single design system; migrate WP content into /careers and /insights.

79% growth, $4.5bn GWP, 560 partners, $1.6bn under Palantir, 25% follow capacity — none visualised.

Fix: Commission a "By the Numbers" scroll module rendered in SVG with restrained motion.

The brand has no recognisable graphic motif (line, mark, gradient, geometric system).

Fix: Develop a single signature device (e.g. interlocking placement-flow lines) and deploy across hero, dividers, social cards.

Buttons carry no brand personality, no motion on hover, no dual-CTA discipline.

Fix: Custom button system with motion on hover; dual-CTA discipline throughout the site.

AI Redesign Prompt — Copy-paste ready

Full design system specification (8 dimensions). Share directly with a design studio or use with any frontier AI model.

Redesign Roadmap — Phased Timeline

| Phase | Window | Deliverables | Cost |

|---|---|---|---|

| Phase 1 — Foundations | Days 1–14 | Domain redirect, JSON-LD, atomic answers, headings, meta architecture, sitemap, OG tags, alt text | £8k–15k |

| Phase 2 — Content & Authority | Days 15–45 | Hero rebuild, /platform page, leadership portrait series, "By the Numbers" strip, six practice page rewrites with named brokers | £45k–75k |

| Phase 3 — Differentiation | Days 46–90 | Underscore interactive module, SVG data viz, signature visual device, employer brand consolidation, Quarterly Outlook editorial system | £70k–120k |

| Total | 90 days | £123k–210k |

Voice Assessment

Current site voice is professional-neutral: "specialist insurance brokers," "we partner with our clients," "decades of experience." The voice is indistinguishable from at least eight other London brokers. Nothing in it suggests a firm that has built the most concentrated AI partnership stack in Lloyd's.

The corrected voice: confident, technical, and editorial. Specific claims with specific evidence. Names of partners. Dates of agreements. The model is a top-tier law firm or a private bank — not a corporate consultancy.

Digital Presence Coherence

McGill is highly visible in trade press (Reinsurance News, Insurance Insider, InsurTech Digital, BusinessWire) and on senior partners' LinkedIn profiles. The owned digital channel captures none of this earned authority. The presence-to-ownership ratio is approximately 5:1 in favour of unowned channels — the highest imbalance in the named peer set.

| Channel | Status | Reach | Coherent with brand? |

|---|---|---|---|

| LinkedIn (company) | Active | ~16,490 | Partial |

| LinkedIn (Steve McGill CBE) | Active | High | Strong |

| Twitter / X | Limited | Low | Weak |

| YouTube | Present in nav | Limited | Weak |

| Glassdoor | 4.6/5.0, 98% recommend | 55 reviews | Strong — undersurfaced |

| Press / PR | Strong | 6 announcements / 14 months | Strong but not aggregated on owned site |

Positioning Opportunity

The market opportunity is a one-line repositioning: from "specialist insurance broker" to "the Lloyd's specialty broker built around an AI placement platform." The supporting evidence is already in earned media; it just needs to be assembled on the owned site.

Digital narrative test (six-second rule): A senior diligence analyst given six seconds on the homepage today describes McGill as: "competent specialty broker, generic positioning, professional but unremarkable." The same analyst given six seconds on the proposed homepage: "Lloyd's broker with an AI platform — Palantir, Salesforce, Google, AIG involved." That delta is the entire brief.

Homepage Copywriting Brief

Use with any frontier AI model or brief a senior copywriter directly.

Format Gap Grid

| Format | McGill | Howden | Miller | Lockton | Tysers | Ryan Specialty |

|---|---|---|---|---|---|---|

| Atomic answer blocks | None | Yes | Partial | Yes | Partial | Yes |

| JSON-LD Organization schema | None | Yes | Yes | Yes | Partial | Yes |

| Named-partner author bylines | None | Yes | Partial | Yes | None | Yes |

| Practice-page named senior contacts | None | Yes | Partial | Yes | Partial | Yes |

| Case studies on practice pages | None | Yes | Partial | Yes | Partial | Yes |

| Original data publications (annual) | None | Yes | Partial | Yes | None | Partial |

| Interactive product demonstration | None | Partial | None | Partial | None | Yes (RT Connector) |

| Editorial portrait photography | None | Yes | Yes | Yes | Partial | Yes |

| Quarterly market outlook publication | None | Yes | Partial | Yes | None | Partial |

| Routed CTA discipline | None | Yes | Partial | Yes | Partial | Yes |

| Total green | 0/10 | 9/10 | 4/10 | 9/10 | 1/10 | 8/10 |

Conversion Infrastructure Today

- A generic contact form with no context routing

- Region-based contact cards (where rendered)

- A LinkedIn message to Steve McGill or a named partner

There is no segmented path for carriers, large corporates, mid-market clients, talent applicants, or media. Every visitor is treated identically — which means no visitor is treated optimally.

Measurement Gap

GTM is installed but the measurement layer is shallow. There is no visible funnel, no conversion event taxonomy, and no source attribution. The reporting capacity exists in the framework — it is unconfigured.

90-Day Growth Roadmap

| Window | Actions | Target Outcome |

|---|---|---|

| Days 1–14 | HubSpot/Salesforce form integration with UTM + source tracking; GA4 events for every CTA click; Search Console configuration; Open Graph + Twitter card metadata | Full attribution model live |

| Days 15–45 | Two routed CTAs across the site; segmented enquiry forms; "Speak to this team" CTA on every practice page with a named senior broker | +30–50% qualified enquiry rate |

| Days 46–90 | Full attribution model; cohort analysis on inbound by source; quarterly board-level digital scorecard | 23 inbound qualified enquiries / quarter |

Action Map · Visual Plot

Every candidate action plotted by effort (x) and impact (y). Size represents cost. Colour represents priority tier.

M8 Impact / Effort Matrix

- Domain redirect (mcgillandpartners.com)

- JSON-LD schema implementation

- Atomic answer blocks (all pages)

- Interrogative headings rewrite

- Meta architecture + sitemap + alt text

- /platform page — full AI stack narrative

- Homepage hero rebuild

- Editorial portrait series

- Underscore interactive module

- SVG data visualisation

- OG tags + social card images

- Author bylines on insights posts

- FCA reference upgrade in footer

- Full CMS replatform

- Design language across employer brand subdomain

- Rebuild of wp.mcgillpartners.com (defer)

Top 5 Priority Actions

| # | Action | Impact | Effort | Cost | Owner | Window |

|---|---|---|---|---|---|---|

| 1 | Acquire and 301-redirect mcgillandpartners.com to mcgillpartners.com | Critical | Low | £2–8k | CMO + IT | 7 days |

| 2 | Implement JSON-LD schema (Organization, Person, Service) across canonical pages | Critical | Low | £4–8k | CMO + dev | 14 days |

| 3 | Rewrite homepage hero with technology positioning + atomic answer + partner logo bar | Critical | Medium | £15–30k | CMO + brand | 30 days |

| 4 | Build /platform page — Underscore, Auton, Agentforce, AIG-Palantir, Bellwether, Artificial Labs with metrics | Critical | High | £35–55k | CMO + product marketing | 45 days |

| 5 | Atomic answers + interrogative headings across all six practice pages and /who-we-are | High | Low | £6–12k | CMO + copy | 21 days |

AI Execution Brief Copy & Paste

Paste this prompt into Claude, ChatGPT, or Gemini to brief an AI assistant on the full programme. The model will return a phased delivery plan, content drafts, and per-page change specs aligned to the priorities above.